Complex looks sexy

A continuation from last week's post on investing lessons from a 10 year old

This post is a continuation of last week’s post on investing lessons from a 10-year-old child.

It’s important that you go through that piece before proceeding with this one to get the nuance of not judging a book by its cover.

Let’s take one complex company and one simple company while keeping in mind the unit economics of the girl running the lemonade stand from last week’s post.

Frontline Numbers Company (A hypothetical example, I let my imagination run wild)

Frontline Numbers Company is a well-established healthcare company based, engaged in the development and manufacturing of various healthcare products.

Scenario: Over the past few years, Frontline Numbers Company has been investing heavily in research and development (R&D) to create new, innovative drugs and expand its product portfolio. As a result of these investments, the company has seen a significant increase in its reported profits due to accounting principles related to revenue recognition and amortization of R&D expenses over time.

Explanation: The company's profits grew rapidly due to accounting practices, such as recognizing revenue from sales of new drugs and amortizing the R&D expenses over several years. As per accounting standards, these practices allow the company to show profits on its income statement but the cash flows may be pointing to a completely different picture.

Regardless of whether you knew this company was tweaking it’s profit numbers or not, had you gone to the cash flow statement, chances are you would not have been enamored by the profitability numbers because you cannot make these adjustments in the cash flow statement.

In reality, the company may be facing challenges in converting its reported profits into actual cash.

This situation can arise because of various factors, such as extended credit terms offered to customers, slow collections from customers, high inventory levels, or substantial investments in fixed assets.

It is not the fault of the company, it is the fault of the investor who is not digging deeper to get more answers.

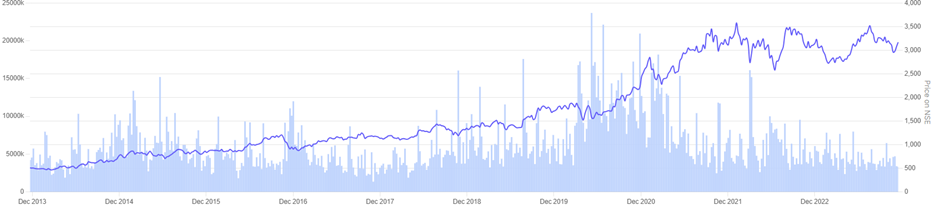

This is the chart of Frontline Numbers Company

Explanation of the Chart:

The chart represents the stock performance of Frontline Numbers Company over four years from 2019 to 2022.

Now do not get me wrong, it is proven that the long-term stock price performance converges with the earnings growth of the company but the profit only means something if it going to get converted into real cash.

The chart shows an upward trend in the stock price, indicating that investors initially responded positively to the reported profit growth and optimistic prospects of the company due to its accounting practices.

The steep increase in the stock price from 2020 to 2021 corresponds to the period when Frontline Numbers Company was reporting significant profit growth due to revenue recognition and R&D expense amortization.

The company had also announced the planned launch of a new drug, news that investors took to very keenly.

However, towards the latter part of 2021 and extending into 2022 going into 2023, investors and the market start to realize that the reported profits have not translated into equivalent cash flow growth and may not do so anytime soon.

This realization leads to a fall in the stock price by almost 60% over a short period.

Now, let's examine the Boring Slow Grower (Another fictional company)

This company typically stays out of the headlines for any sensational news and maintains consistent growth. It may not be captivating enough to attract attention or spark investor interest.

Investors are often not enticed by the gradual growth of Boring Slow Grower. These companies are rarely found in individual investor portfolios, and even if they are included, they typically constitute a minimal portion of the overall portfolio because of their lack of glamour.

ESPECIALLY considering where the market is today, these companies would not even feature

Observe a boring slow grower’s chart in the short term of 3 years, with barely any movement and even flat performance despite posting strong fundamental numbers and healthy conversion of profits into real cash.

Zoom out now and see the performance for 10 years for Boring Slow Grower:

100 Rs invested into boring slow grower would have become 1000 Rs in 10 years

If you do not understand the health of the company’s financials then why would you invest your hard-earned money?

Frontline numbers can create an optical illusion for the investor.

John Bogle rightly points out that:

“Sooner or later, the rewards of investing must be based on future cash flows. The purpose of any stock market, after all, is to simply provide liquidity for stock in return for the promise of future cash flows, enabling investors to realize the present value of a future stream of income at any time.”

Markets determine the prices of stocks just like any other financial asset in the long term, in two ways:

1. Market prices respond to changes in the company’s prospects for cash flow.

2. Market prices reflect cash flows well into the future.

Conclusion

Never judge a book by its cover.

Relevant Reads from my Blog: